I’m going to talk about the main steps that go into the settlement demand and settlement process in a personal injury case.

This article assumes that someone else’s negligence caused your injury.

Table of contents

- Make sure the Accident is Reported

- Try to Settle Before It’s Too Late to Sue…If Appropriate

- Make Sure Case Is Ready To Be Settled

- Find Out Each Insurance Company’s Limits

- Don’t Rely on Insurer to Tell You if Other Insurance Exists

- Request Your Medical Records, Bills and Other Documents

- Send The Insurers Medical Records and Bills

- Send the Adjuster Photos of Evidence that Helps Your Case

- Get Doctor to Say What Your Your Future Medical Treatment and Expenses Will Be

- Make a Spreadsheet of Your Medical Bills and Out of Pocket Bills

- You Need to Know How Much Your Health Insurer Paid

- Verbally See How Much Health Insurers Will Settle For

- Write a Demand Letter and Send it to the Insurers

- Try to Negotiate a Settlement

- If Case Settles, Send the Adjuster Your Proposed Release

- Settle Your Health Insurance Liens and Other Bills

Make sure the Accident is Reported

Make sure that you report your accident to the police. In fact you are often required too. Section 316.065, Florida Statutes, requires the driver of a vehicle involved in a crash involving injury or death to a person, or at least $500 estimated vehicle or property damage to immediately contact local law enforcement.

Don’t allow the other driver to drive off without having the police come to the scene.

Why?

As you’ve seen, you are required to in most cases. But that’s not the only reason.

The driver, or other person or company that was at fault may later change their story of what happened. They may later blame you! If you don’t report the accident, and their were no independent witnesses, you may have a difficult case. This means that the other person’s insurance company may deny your claim or offer you less the fair value of the case (had your reported the accident).

One phone call to the police from the accident scene may save you thousands of dollars when it comes to settlement.

If you’re involved in a minor accident

Try to Settle Before It’s Too Late to Sue…If Appropriate

Before we get into the settlement process, you should note that there is a time limit to sue.

For example, in most cases in Florida, you have four years to sue. In certain cases, you need to give a notice of claim much earlier than the 4 year deadline to sue.

In cruise ship injury cases, you often only have 1 year to sue. If you miss the deadline to file a lawsuit in any of personal injury case, you lose your case.

Make Sure Case Is Ready To Be Settled

When thinking about settlement, you need to make sure that your case is ready to be settled.

The two most common events that make a personal injury case ready for settlement are:

- you’re finished with your medical treatment; or

- the value of the case exceeds all available insurance coverage in the case.

Prior to settling the case, you need to make sure you know every single insurance company that may pay for the case.

Find Out Each Insurance Company’s Limits

You also need to know the insurance company limits.

It’s important to know this information because if your case becomes more valuable than the insurance limits, your case is ready for settlement.

If you don’t know those insurance limits, then you’re not going to know whether your case is more valuable than those insurance limits.

Don’t trust what the insurance company tells you the insurance limits are. Get it in writing.

In Florida, you can request this is writing. The insurance company has to provide that to you in writing.

Ask the Responsible Parties to Preserve Evidence

Be sure to ask the responsible parties evidence. Your request needs to be in writing. If the other side destroys evidence and you never asked them to preserve it, you could lose your case.

In some cases, you may need to get out to the accident scene quickly to take photos of the hazard.

Don’t Rely on Insurer to Tell You if Other Insurance Exists

Even if the insurance company tells you that they aren’t aware of any other insurance policies that may pay the claim, don’t take their word for it. There have been times where we’ve been able to find additional insurance, even though the insurance company, in writing, under oath, told us that they weren’t aware of any additional insurance.

In one case, the insurance company, USAA, told us that there was $100,000 of bodily injury (“BI”) insurance coverage from the careless driver that caused our client’s injury.

Only after pressing USAA, did they become aware of an extra $1,000,000 insurance policy at play. I ended up recovering an additional $100,000 from that extra $1,000,000 policy.

This was in addition to the $100,000 of USAA’s BI liability insurance. The case settled for $200,000.

Request Your Medical Records, Bills and Other Documents

As soon as possible after your accident, you need to request every single piece of documentation in your case. This includes your medical records and medical bills.

Even if the insurance company sends you an authorization and tells you that they’re going to request your medical bills and records, don’t rely on them.

When thinking of which bills and records that you need to request, start from the events that happened immediately after the accident. If you take an ambulance to the hospital, you need to request those ambulance medical bills and records.

If you get medical treatment at the hospital, you need to request your hospital bill and record, and your emergency doctor’s bill.

There will be a separate bill for the ER doctors and the hospital. I’ve never seen them as the same bill.

If X-rays or CR scans were taken of you, you should request the radiology bill. If blood work was done, request the pathology bill.

There may be other bills as well. If you had surgery, request the surgeon’s bill.

Send The Insurers Medical Records and Bills

You should continue giving the insurance for the at-fault party all of your medical records and bills. This is so they can properly set the reserve, which is the amount of money they set aside to pay your claim.

Don’t just give the adjuster your bills and records at the last-minute. If you wait, they may need more time, and sometimes a lot more time, to get settlement authority to pay your case.

The goal is to get fair value for your case as soon as possible. In order for this to have the highest chance of happening, you need to continuously send the insurance company(ies) all of your medical information.

Send the Adjuster Photos of Evidence that Helps Your Case

In order to get your case ready for settlement, you need to send the insurance adjuster all photos in your case that help support your claim.

If you were in a car accident or truck accident, send the insurance adjuster pictures of the property damage, particularly if there was a lot of damage.

The higher the amount of damage, all things equal, helps the settlement. Also, if you suffered injury, send the adjuster photos of your bruising, cuts, hardware in your body, outside your body, and anything else that may help.

Send Photos Immediately (Don’t Wait)

Send these to the insurance company sooner rather than later. You want your claim to stick out in the adjuster’s mind.

The more documents you send them, the more the adjuster is forced to look at your claim. This assumes that the documents are helpful to your case.

The more time they spend on your claim, the better they get to know it and you. Take pictures, photos, of the incident scene if it’s appropriate.

This photo below is from a trip and fall case where my client tripped and fell on this vinyl landscaping edge.

I went out to the scene very shortly after and fortunately, it hadn’t changed. I took a photo of the alleged hazard to show the adjuster what my client caused her to trip and fall.

Her fall resulted in her getting stitches below her eye. She also had a minor wrist injury. If I did not take that photo, the business may have denied that there was a hazard on its property.

The business may tell their insurance company there was nothing wrong. They may fix it.

The insurance adjuster may choose to believe them. If you can get the adjuster photos as soon as possible, and they’re helpful to your claim like this one, it may help you get a settlement that is closer to the full value of the case.

This case settled for $18,000. There’s a strong likelihood that without these photos, the case may have not have settled for that much.

It may have settled for much less. It may have not even settled.

Send the Adjuster Images of Your Injuries and X-rays

You want to send the insurance adjuster the actual CT scans and X-rays and MRIs of your injuries if you have them.

For example, the above image is of the large lower leg bone – the tibia. It shows a fracture. In this case, we requested this film from the emergency room.

We quickly sent it to the insurance company for the careless driver that hit my client while he was a pedestrian. This “forces” the adjuster to look at the image.

He or she sees the significance of your injury. It helps them, possibly, assign more money to the case.

Get Doctor to Say What Your Your Future Medical Treatment and Expenses Will Be

If you’re going to need more medical treatment in the future, be sure to have a doctor write down:

- the type of medical treatment that you’re going need in the future; and

- how often you’re going need it; and

- the cost of it.

I settled a case for $445,000 where an 18-wheeler hit a motorcycle rider. The tractor part of the truck hit my client.

We asked the doctor to write down what he thought my client’s future medical costs would be.

On many of my phone calls with the adjuster, I would mention the surgeries that my client’s doctor said that he will need in the future. I would tell him the cost of them.

That may have helped me get this $445,000 settlement, where my client fractured his tibia, and had surgery.

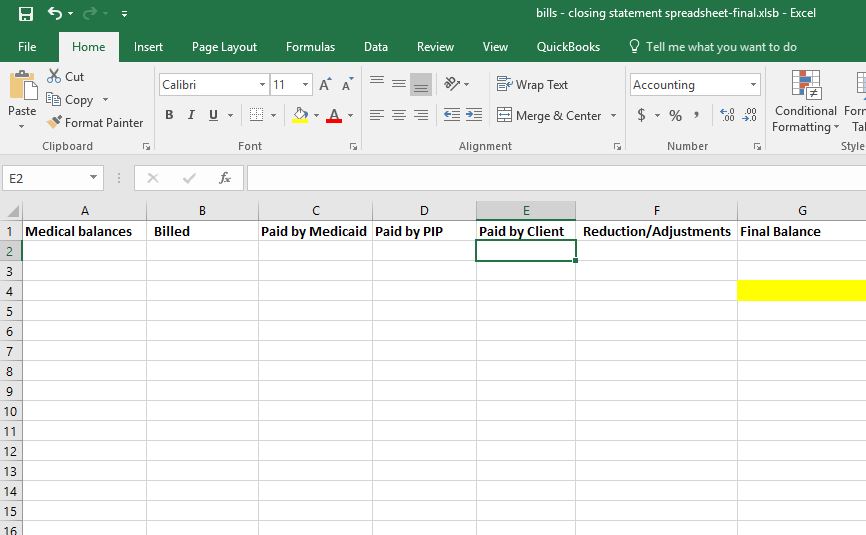

Make a Spreadsheet of Your Medical Bills and Out of Pocket Bills

I use a spreadsheet to list the:

- dates of treatment

- type of treatment

- total bill charges

The general rule of thumb is the higher your total bill charges, all things equal, the higher the full settlement value of the case. I also list the amounts paid by health insurance, Medicaid or Medicare, the out of pocket charges that my client owes, as well as the amounts that were paid.

In Florida, for example, you’re entitled to recover the out of pocket medical charges. If your health insurance company, or Medicaid or Medicare paid for some of your medical bills, you’re also entitled to recover that money.

If you settle your personal injury case, you then must reimburse these medical “insurances” at least a certain percentage of the amount that they paid for related care.

A spreadsheet allows you to know all of your medical bills. If you get an additional bill, or one of your bills is later reduced or adjusted, all you have to do is change one cell and it adjusts everything.

You want to have this spreadsheet open when you’re talking with the insurance adjuster. Insurance adjusters are very busy.

It makes it easier for them to discuss your case if you’re prepared. The more prepared you are, the more it may help your claim.

You need to know exactly what your out of pocket costs are so that you can estimate the fair value of your claim.

You Need to Know How Much Your Health Insurer Paid

If you have health insurance, Medicare and Medicaid, or some other type of major medical plan that will pay your bills, you need to know how much they paid.

They are likely going to assert a lien. They are going to make a claim against your recovery in your personal injury case. Early on in your claim, start talking with the health insurance plan about how much they are willing to take to settle their lien.

Sometimes they are generous. For example, Medicare and non-self funded ERISA health plans must reduce by your pro-rata attorney’s fees and costs.

On the other hand, Florida Medicaid has a particular settlement formula that makes sure that the injured person gets a certain percentage of the settlement in his or her pocket.

Your negotiation power will a medical insurer depends, in part, on whether your health plan is self-funded. This will likely be determined by the size of your employer, if your insurance is through them.

If you work for a huge private company, with thousands of employees, you likely have a self-funded health plan. This means the health plan usually has the leverage in negotiations.

Example where a self funded health plan can be fair when reducing its lien claim

Sometimes a self funded health plan will be fair when reducing its lien. let me give you an example.

I settled a slip and fall case for $300,000. My client worked for a huge employer (HCA). He had self-funded health insurance through his employer.

The self-funded health plan paid around $75,964 to the medical providers who treated him for his slip and fall.

Now:

The health could have required me to pay them back the entire $75,964. However, they agreed to accept $48,134 as the payback settlement amount. That put an extra $27,830 in my client’s pocket! My client’s health plan was very generous.

There are other exceptions where a self funded health plan may reduce its lien. There are also certain letters that you need to send to your health plan.

If you’re working for a large business that has a self-funded health plan, send this letter to the plan administrator. They can incur certain penalties by not timely responding to your request for their lien.

This can give you leverage when it’s time to negotiate their lien.

There are two big parts to the personal injury case. One is reaching a settlement with the at-fault parties.

The second part is the back end, which is trying to get all your health insurance bills and liens knocked down.

Verbally See How Much Health Insurers Will Settle For

We typically ask, in a phone call, each health insurer how much money that will settle for so that I can estimate the amount that my client will be receiving. It’s very important to know the health insurance lien.

For example, let’s say you settle your case for $100,000, but your health insurance paid $100,000 in medical bills. In some instances, the health insurer may demand that you pay them the entire $100,000.

This is more likely to happen if you work for a huge private employer that is not willing its plan.

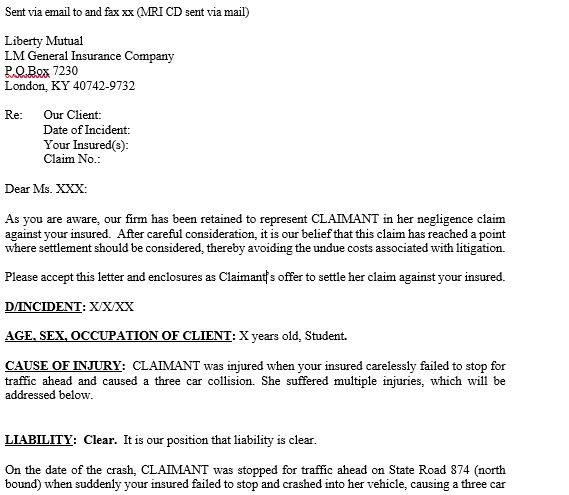

Write a Demand Letter and Send it to the Insurers

Here is part of a settlement demand letter that I used in a car accident case:

A demand letter is essentially a letter with enclosures that includes your medical bills, records and photos that support your claim. Even if you’ve sent the appropriate liability insurers these documents, you may want to also include those in your demand package.

You’re generally want to give the insurance company a time limit to respond so that they put it in their calendar and they respond within that time limit. If you don’t give them a time limit, there’s a higher chance that they’re going to delay making you an offer.

The demand package and letter is your time to explain how this incident has affected your life. You may want to include photos of yourself before the accident, and photos that shows any changes after the accident.

If you’re a runner, for example, and now you’re unable to run or you have difficultly running since the accident, send the insurance adjuster some pictures showing that you were able to run in marathons or the awards that you received.

Then, perhaps, send them a short video or photos of you that show that you have difficulty walking now. That can help your case stand out in the insurance adjuster’s mind and it can show that your life has been negatively affected.

In Florida, for example, if you can show that someone else’s carelessness caused your injury and you lose enjoyment of life, you’re entitled to recover compensation for that.

Tougher to Get Pain and Suffering Money in Most Florida Car Accident Cases

In most Florida auto accident cases, the standard to get money for pain and suffering is higher. You typically need a permanent injury in these cases.

You want to make sure that the insurance adjuster knows exactly how the accident has made your life tougher. You can put it in writing. You can also communicate it with them over the phone.

In some demand letters, you may want to say that your demand is dependent on there being no other insurance available. In Florida, when making a claim against a BI liability insurer, you may want to include language that says this demand is subject to the uninsured motorist insurer(s) waiving their right of subrogation.

Try to Negotiate a Settlement

When negotiating your case, you want to make a high demand. However, don’t make too high of a demand. I’ve had cases where my clients insisted that our demand was very high. This can delay settlement.

For example, let’s say that you make a $500,000 demand, but your case is only worth $197,500 or so. The insurance company may make a few counter offers if you only reduce your demand slightly.

However, at some point the insurance company may stop making settlement offers. In addition, there is a chance that the insurance adjuster may make a smaller “final” offer that he would make if you lowered your settlement demand much more.

As an example, let’s say that he offers you $150,000. He may tell you that he can’t increase his offer. There’s a chance that the adjuster is able to offer you more money, but it’s possible that he won’t because your demand is so high.

The adjuster may think to himself that increasing his offer is a waste of time because there will still be such a big difference between your demand and his offer.

Making the right settlement demand amount is very important in a case.

If your first settlement demand is one that the insurance company will accept, it’s probably too low. The exception to this rule is if there is limited insurance coverage available.

In most cases, you should typically demand above what you’re willing to settle for. This gives you room to negotiate.

Also, when you’re negotiating with an insurance adjuster, do not believe what they tell you. I’ve heard insurance adjusters for the careless party tell me that they were giving me their final offer. Then, a week later they increase their offer by $5,000 or $10,000.

If an insurance adjuster won’t increase his offer, sometimes you want to speak with the claims manager. But understand that personal injury claims usually involve negotiation.

The first offer that the insurance adjuster gives you is usually not his/her final offer. An exception to this, is if they’re offering you their policy limits and that’s all the money that’s available.

However, even in policy limits cases, you may be able to squeeze out a little bit of more money from their insured.

If Case Settles, Send the Adjuster Your Proposed Release

If you’re able to settle your case, the insurance company usually sends you one settlement check. They generally don’t send more than 1 settlement check.

They will require you to sign a settlement release. Essentially, the release says that you agree to give up all claims against their insured and/or the insurer for the rest of your life.

You may want to send them a proposed settlement release. There are a few rights that you don’t want to give up.

You don’t want to give up your right to sue any other parties. For example, let’s say you had surgery and the doctor put in hardware inside your body. In Florida, if you just sign the insurance company’s release, you may be giving up your right to sue the hardware manufacturer if that product turns out to be defective. You may also be giving up your right to sue a doctor if it turns out that he or she was careless.

You also don’t want to give up your right to make claims against your health insurer, or Medicare, Medicaid, etc.

Treat the release very seriously.

Settle Your Health Insurance Liens and Other Bills

After you settle with the insurance company, it’s time to finalize your liens with your health insurance company and other medical insurers.

If you have a lawyer

If Appropriate, Pay Medicare and Medicaid to Avoid Jail time

If you fail to pay Medicare or Medicaid, for example, you can be thrown in jail and face huge penalties. Your health insurance company could possibly reverse the payments that they’ve made or cut off your future health insurance care if you stiff them.

Early on in most cases, you should start talking with your health insurers about how much they’ll accept to satisfy their lien. This is so that when the case settles, you’re in a better place to negotiate the lien.

If you don’t know how much the health insurer will accept, then you lose your negotiating power because the health insurer may not reduce the lien.

If you start talking with the health insurer about settlement early on, and they’re requesting to be paid back an amount that will eat up the entire settlement, you can always decide not to continue with your personal injury claim.

If you tell them this, they may become more willing to negotiate their lien.

Please let me know your comments. Do you agree with the settlement process and demand the way that I’ve described it?

I want to represent you if you were hurt in an accident in Florida, on a cruise ship or boat.

Call Me Now!

Call me now at (888) 594-3577 to find out for FREE if we can represent you. We answer calls 24 hours a day, 7 days a week, 365 days a year.

No Fees or Costs if I Do Not Get You Money

We speak Spanish. Learn more about us. Check out my law firm reviews.