Is an insured tortfeasor is entitled to a set-off for Personal Injury Protection (PIP) when the claimant is uninsured in violation of Florida’s no-fault laws?

Don’t panic if you don’t understand this question. I will explain this question using a simple example further below.

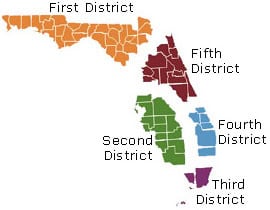

Car Accidents in Southeast Florida; PIP Setoff

The answer to the above question is that a careless driver gets a PIP setoff in that circumstance if you the auto accident occurred in the counties governed by the Third and Fourth District Court of Appeal.

The cases that say this are Cases v. Gray, 894 So. 2d 268 – Fla: Dist. Court of Appeals, 3rd Dist. 2004; Holt v. King, 707 So.2d 1141, 1142 (Fla. 4th DCA 1998).

Florida 3rd DCA handles appeals for Miami-Dade and Monroe County. Florida’s 4th DCA handles appeals from Palm Beach, Broward, St. Lucie, Martin, Indian River, and Okeechobee Counties.

Car Accidents in West and Central Florida; No PIP Setoff

Warning! The answer to the above question is no to cases that are in counties governed by Florida’s second and fifth district court of appeals.

There are fourteen counties in the Second District, which include: Pasco & Pinellas, Hardee, Highlands, Polk, DeSoto, Manatee, Sarasota, Hendry, Hillsborough, Charlotte, Glades, Collier and Lee.

Florida’s Fifth District Court of Appeal is comprised of Hernando, Lake, Marion, Citrus and Sumter Counties, Flagler, Putnam, St. Johns and Volusia Counties, Orange and Osceola Counties, Brevard and Seminole Counties.

Facts of Holt v. King

In Holt, Phylesia King, sued Leo Holt, for personal injury and damages resulting from an automobile accident. Florida’s Fourth District Court of Appeal of Florida issued its ruling on February 18, 1998.

This case is still good law. If Florida no-fault laws require you to have insurance, and you do not have it, you need to know this case.

The lawsuit also named Midland Risk Insurance Company, King’s own insurance company, claiming that Midland “wrongfully refused and continues to refuse to pay for claimant’s covered losses.”

However, the trial court granted Midland’s Motion for Final Summary Judgment (for permanent dismissal), concluding that King’s policy had been cancelled three days prior to her accident due to her failure to pay her insurance premium.

Prior to trial, King filed a motion (request) to strike Holt’s affirmative defense that he was entitled to a set-off for Personal Injury Protection payable to King. The motion pointed out that the trial court had granted Midland’s motion for final summary judgment, finding “conclusively that the Plaintiff did not have any personal injury protection benefits at the time of the accident.”

King’s motion contained the following language:

“That since the Plaintiff did not have any valid personal injury protection benefits available to her, then pursuant to Ward v. Nationwide, 364 So.2d 73 (Fla. 2d DCA, 1978), Stevens v. Renard, 487 So.2d 1079 (Fla. 5th DCA, 1986) and Erie Insurance Co. v. Bushy, 394 So.2d 228 (Fla. 5th DCA, 1981), there would be no set-off.

The trial court granted King’s motion, stating:

“Granted. As the court is bound by Ward v. Nationwide, 364 So.2d 73 (Fla. 2nd DCA 1978); Stevens v. Renard, 487 So.2d 1079 (Fla. 5th DCA 1986); Erie v. Bushy, 394 So.2d 228 (Fla. 5th DCA 1981) and no 4th DCA opinion.

Following jury selection, but prior to opening statements, Holt admitted negligence and causation. However, the trial proceeded for the purpose of determining damages. Among the disputed damage issues was whether King had suffered a permanent injury so as to entitle her to damages for pain and suffering.

Following the testimony of several doctors, the jury determined that King was entitled to $8,407.00 for past medical expenses and lost earnings, but that she had not suffered any permanent injury. The trial court then entered final judgment in favor of King for $8,407.00.

Hold filed a post-trial motion, requesting yet again a PIP set-off of 80%, which would result in a damage award of $1,681.40.

Holt took the position that King, being uninsured at the time of the accident, was considered to be self-insured under Florida law for the purpose of PIP coverage and was, therefore, responsible for the statutory minimum of 80% of her own medical expenses.

The trial court, however, ultimately denied Holt’s requested set-off. Holt appealed.

Florida Statutes section 627.733, entitled Required Security, requires all motor vehicle owners to maintain “no-fault” automobile insurance covering, among other items, 80% of the insured’s own medical expenses. See §§ 627.733(1), (3)(a), 627.736(1)(a), Fla. Stat.

Every vehicle owner who gets the mandatory no-fault coverage is afforded a limited exemption from tort liability:

“Every owner, registrant, operator, or occupant of a motor vehicle with respect to which security has been provided as required by ss. 627.730-627.7405 … is hereby exempted from tort liability for damages because of bodily injury, sickness, or disease arising out of the ownership, operation, maintenance, or use of such motor vehicle in this state to the extent that the benefits described in s. 627.736(1) are payable for such injury, or would be payable but for any exclusion authorized by ss. 627.730-627.7405, under any insurance policy or other method of security complying with the requirements of s. 627.733, or by an owner personally liable under s. 627.733 for the payment of such benefits, unless a person is entitled to sue for pain, suffering, mental anguish, and inconvenience for such injury under the provisions of subsection (2).”

§ 627.737(1), Fla. Stat.

As this law states, the tort exemption is effective as to non-permanent injuries to the extent that PIP benefits are payable for such injuries or would be payable by a vehicle owner personally liable for the payment of such benefits under section 627.733. A vehicle owner is personally liable for PIP benefits under section 627.733 when he or she fails to obtain the mandatory coverage:

“An owner of a motor vehicle with respect to which security is required by this section who fails to have such security in effect at the time of an accident shall have no immunity from tort liability, but shall be personally liable for the payment of benefits under s. 627.736. With respect to such benefits, such an owner shall have all of the rights and obligations of an insurer under ss. 627.730-627.7405.”

§ 627.733(4), Fla. Stat.

Under the plain language of these statutes (laws), the appeals court said that King, as an uninsured driver, was self-insured to the extent of 80% of her own medical expenses. Thus, Holt, an insured tortfeasor, was entitled to an exemption from tort liability to that same extent.

The appeals court said that the cases relied upon by King are either distinguishable or have been superseded by later Supreme Court authority.

The case of Ward v. Nationwide Mutual Fire Insurance Co., 364 So.2d 73 (Fla. 2d DCA 1978), relied upon by King and the trial court, did not involve a tortfeasor‘s right to a set-off pursuant to the statutory tort exemption, but, rather, involved the question of whether public policy relieves an insurer of his contractually-undertaken duty to a claimant when the claimant has failed to comply with the no-fault laws.

In Ward, as in this case, the injured claimant did not have the mandatory automobile insurance on her own vehicle. However, she was injured while occupying another person’s vehicle, which was insured. Under the vehicle owner’s insurance policy, the claimant was entitled to PIP coverage.

In ruling in favor of the claimant, the Second District applied the general principle of Florida law that a party is not relieved of its contractually-undertaken responsibilities simply because the other party has violated the law in some way.

Like Ward, the case of Erie Insurance Co. v. Bushy, 394 So.2d 228 (Fla. 5th DCA 1981) involved an insurer’s claim that the injured plaintiff’s failure to obtain the mandatory no-fault insurance coverage excused the insurance company from its contractually-undertaken duty to provide coverage. Relying on the contract-based rationale of Ward, the Fifth District held:

“We reject appellant’s second point on appeal that it is entitled to a “set-off” of $5,000.00 because the claimant failed to carry no fault insurance, and therefore was a self-insurer under Florida Statutes, section 627.733(1). Ruling an owner of an uninsured motor vehicle liable as a self-insurer for damages suffered from an insured driver would avoid the express insuring contract provisions in Erie’s liability policy. It should make no difference to Erie under its liability policy whether the injured person has or does not have insurance. Ward v. Nationwide Mutual Fire Insurance Company, 364 So.2d 73 (Fla. 2d DCA 1978).”

The appeals court is of the opinion that the contract-based rationale of Ward and Erie does not apply in this case because Holt in this case undertook no contractual duty to insure King.

However, the final case relied on by King, Stephens v. Renard,487 So.2d 1079 (Fla. 5th DCA 1986), like the instant case, involved a tortfeasor’s right to a set-off against an uninsured claimant.

Relying on Erie, Stephens ruled that it was error to reduce a damage award based on the claimant’s failure to obtain the statutorily required personal injury protection.

Since the decisions in Ward, Erie, and Stephens, the Florida Supreme Court has addressed similar issues in the cases of Mansfield v. Rivero, 620 So.2d 987 (Fla. 1993), and Hannah v. Newkirk, 675 So.2d 112 (Fla.1996).

In Mansfield, the injured plaintiff had the necessary insurance coverage but apparently waived her right to receive her PIP insurance proceeds, choosing instead to collect from the tortfeasor. However, the Supreme Court ruled that the tortfeasor was entitled to a set-off:

“To accept the district court’s holding in this case that the tortfeasor was not entitled to a set-off would, in effect, nullify a fundamental part of the no-fault law. As noted, the no-fault statutory scheme sets up a means by which an injured party recovers most of his or her out-of-pocket expenses from his or her own insurer, where the injury fails to reach the permanent injury threshold found in section 627.737(2).

The district court’s holding that would allow an injured person to waive his or her rights to receive insurance benefits and sue the tortfeasor would effectively nullify and repeal the personal injury protection benefit scheme set forth in the no-fault law by the legislature.”

The case of Hannah v. Newkirk, 675 So.2d 112 (Fla.1996), further supports Holt’s entitlement to a set-off in this case. In Hannah, the Supreme Court ruled that a PIP set-off properly includes not only the amount of PIP insurance proceeds received, but also the amount of any deductible elected by the plaintiff.

Hannah Case Was Decided Before the Statute Removed No Deductible Recovery Language

The Hannah case was decided before the part of the statute (law) that said that the claimant couldn’t recover a deductible was removed. In 2003, the language was removed from Statute 627.739.

In Hannah, the court reasoned that, “in electing a deductible an insured party pays a lower insurance premium and becomes a self-insurer as to that deductible.” Taking Hannah to a logical and reasonable conclusion, when a party chooses to entirely forgo PIP insurance coverage, she becomes self-insured as to the entirety of the mandatory coverage.

Back to the King v. Holt case…

The appeals court agreed with the more recent Florida Supreme Court cases of Mansfield and Hannah, and ruled that an insured tortfeasor is entitled to a PIP set-off against a claimant who is uninsured in violation of the no-fault laws. Accordingly, it reverse the trial court’s refusal to afford Holt a PIP set-off.

To the extent that this opinion conflicts with the Fifth District case of Stephens v. Renard, and because the following question is one of great public importance, it certified the following to the Supreme Court of Florida:

“Is an insured tortfeasor entitled to a personal injury protection (pip) set-off when the claimant has failed to obtain the mandatory no-fault insurance coverage?”

The Florida Supreme Court has not yet answered this question.

Bottom Line

In this case, King owned a car in Florida. She did not have it insured. In Florida, you are required to insure your car.

Since she did not have it insured, the other driver was entitled to get her total medical bills of $8,407.00 reduced by 80% to $1,681.40. In addition, her medical providers likely had a lien (claim) against that recovery. There likely was no, or very little, money left for King after her doctors were paid from the settlement and her attorney’s fees.

By not having auto insurance, she cost herself $6,725.00. If her medical bills would have been higher, she may have cost herself a lot more money. In smaller cases, it can be a killer if a claimant owns a car but does not have it insured.

Even if King had health insurance, I think Holt would have been entitled to a setoff of 80% of the PIP benefits. So her total judgment (recovery) would have been $1,681.40. She would have likely needed to pay back her health insurer for bills that it paid arising from this accident.

Did someone’s carelessness cause your injury in a Florida car crash or other type of accident?

See Our Settlements

I am a Miami car accident lawyer. I have settled many Florida injury cases. They include, but not limited to, car accidents, truck accidents, motorcycle accidents, bike accidents, pedestrian accidents, taxi accidents, drunk driving (DUI) accidents, accidents involving an Uber or Lyft driver, and many other types of accidents.

I want to represent you if you were hurt in an accident in Florida. If you were injured in another state but live in Florida, we may also be able to represent you.

Call Us Now!

Call us now at (888) 594-3577 to find out for FREE if we can represent you. We answer calls 24 hours a day, 7 days a week, 365 days a year.

No Fees or Costs if We Do Not Get You Money

We speak Spanish. I invite you to learn more about us.