You are here: Home/Auto Accident Claims/ Do Insurers Have to Disclose Insurance Limits? Florida Statute 627.4137

Do Insurers Have to Disclose Insurance Limits? Florida Statute 627.4137

posted on

ACTOR. Not lawyer or employee at my law firm

If someone’s negligence caused your injury, you may want to find out the available insurance limits.

This article generally focuses on Florida personal injury cases. Each state has its own laws regarding disclosure of insurance information.

Before I talk about insurance disclosure laws, I want to explain why insurance disclosure is so important.

The injured person wants to make sure that there is enough insurance to cover his or her injury claim.

Lets’ assume that someone who is injured and has a broken leg. Perhaps he or she has surgery to fix it. He or she will want to make sure that there is enough insurance to pay for his injury claim.

Florida Statute 627.4137 requires an insurer that provides liability insurance coverage to disclose certain information.

The two most common types of liability insurance are:

When doesn’t an insurer have to disclose certain insurance information?

There are certain scenarios where an insurance company does not have to give you insurance information even though your accident happened in Florida. Let’s look at them.

Insurance Policies Issued in a State Other than Florida

The disclosure of insurance information law does not apply to “policies…not issued for delivery in Florida nor delivered in Florida….” Florida Statute 627.401(2)

Example – Out of state insurer doesn’thave to disclose info

Jorge is riding a motorcycle in Hialeah, Miami-Dade County, Florida. A truck cuts him off and hits him.

The trucking company is based in a state other than Florida. The trucking company’s insurance policy was not issued for delivery in Florida.

Thus, the trucking company’s insurer doesn’t have to disclose insurance information pursuant to Florida law.

However, the insurance policy may have been issued in a state that has a law requiring disclosure of certain insurance information. An example of a state that requires insurance information disclosure is Georgia. An example of state that doesn’t require insurance information disclosure is Louisiana.

Doesn’t Apply to Wet Marine and Transportation Insurance

In Florida, wet marine and transportation insurers do not have to disclose insurance information, except ss. 627.409, 627.420, and 627.428.

“Wet marine and transportation insurance” is the part of insurance that includes only:

Insurance upon vessels, crafts, and hulls and of interests therein or with relation thereto. Florida Statute 624.607(3)

Example – Wet Marine Insurer Doesn’t Have to Disclose Info

Joe is on a vessel, craft or hull. Progressive insures it with wet marine and transportation coverage.

Danny carelessly operates it. Joe gets hurt.

I do not believe that Progressive has to disclose insurance information to Joe because the vessel, craft or hull has a wet marine and transportation insurance policy.

Do insurers have to provide insurance information to claimants in Florida?

Each insurer which does or may provide liability insurance coverage to pay all or a portion of any claim which might be made shall give certain insurance information upon written request of the claimant.

How long does a liability insurer have to give a claimant this information?

Within 30 days of the written request of the claimant.

Does a liability insurer have to give a claimant this information if it is not requested in writing?

No. The request must be in writing.

After a claimant has requested certain insurance information in writing, will the adjuster verbally disclose it to the claimant?

In most cases, no. It depends on the liability insurer involved and the particular adjuster who is handling the claim. However, most of the time that insurance company will probably not tell the claimant the policy limits unless it is requested in writing.

Insurance companies are more likely to tell the injured person’s attorney the BIL limits without a written request. But not always.

I’ve had many insurance adjusters refuse to tell me the BIL limits until they received an email or letter from me stating that I represent the injured person. Some adjusters from companies like Progressive, GEICO and many others have done this.

If I’ve dealt with a particular adjuster from the insurance company before, they are more likely to tell me the insurance limits without requiring an email or letter from me.

Does the liability insurer have to give you a statement under oath?

Yes. You should require a statement under oath. The insurer may be more likely to be accurate with its insurance information if it is gives you information under oath.

The insurance company likely meets the “under oath” requirement if it’s representative says:

Under penalties of perjury, I declare that I have read the foregoing [document] and that the facts stated in it are true, followed by the signature of the person making the declaration, except when a verification on information or belief is permitted by law, in which case the words “to the best of my knowledge and belief” may be added. The written declaration shall be printed or typed at the end of or immediately below the document being verified and above the signature of the person making the declaration.

The insurance company can also meet the “under oath” requirement by having the statement notarized.

Does a liability insurer have to give a claimant information with regard to every known policy of insurance, including excess or umbrella insurance?

Yes. Sometimes there are multiple insurance policies that may provide liability insurance coverage.

This may result in your receiving in a claimant receiving additional compensation for his or her personal injury claim.

What information is a liability insurer required to give a claimant if requested in writing?

The insurer must give a claimant the following information with regard to each known policy of insurance, including excess or umbrella insurance:

(a) The name of the insurer.

(b) The name of each insured.

(c) The limits of the liability coverage.

(d) A statement of any policy or coverage defense which such insurer reasonably believes is available to such insurer at the time of filing such statement.

(e) A copy of the policy. Florida Statute 627.4137.

What does a Florida liability insurance disclosure look like?

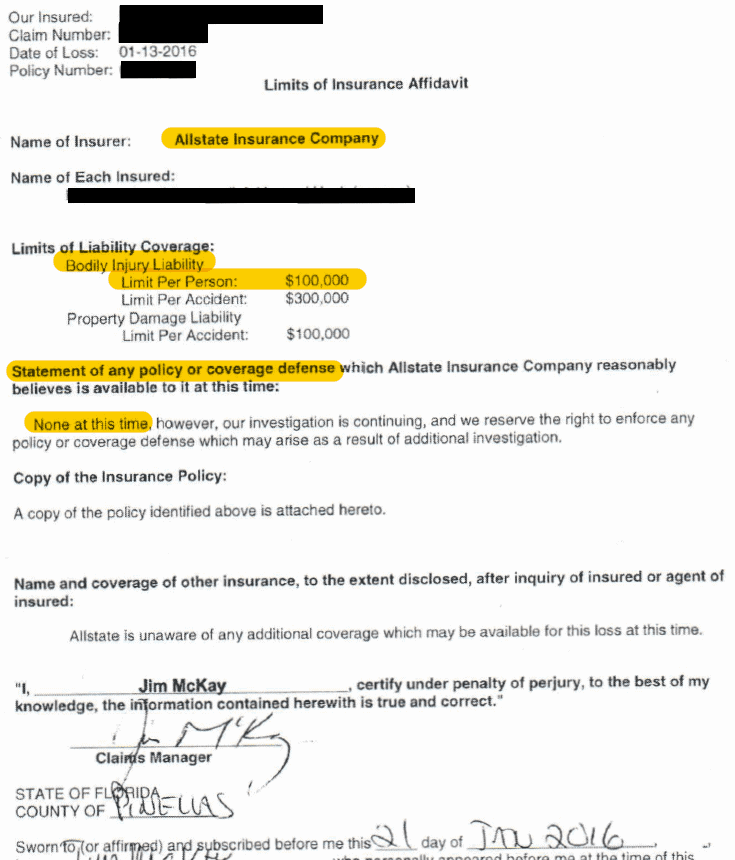

Below, is an example of an Allstate insurance disclosure in a Florida car accident claim. I’ve highlighted some of the more important sections.

Here is a GEICO insurance policy disclosure:

I settled that case for the $100,000 bodily injury liability limits. My client had a broken nose and herniated disc.

She had a nerve block to her lower back, and the doctor recommended surgery.

Here is an Allstate insurance disclosure from one of my many Florida car accident cases.

As you can see above, the insurance disclosure lists Allstate’s statement of policy or coverage defenses. The insurance disclosure is required to tell you what the company’s coverage defenses are.

For example, an insurance company can try to deny coverage if an excluded driver was driving the car.

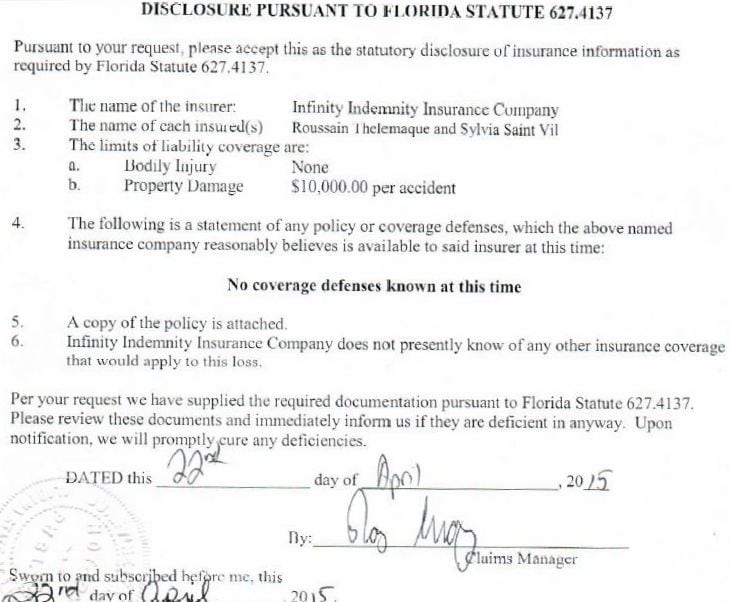

Here is example of a written insurance disclosure from Infinity Insurance Company.

What happens if a liability insurer won’t give a claimant the insurance information that was requested in writing?

Cheverie v. Geisser, 783 So.2d 1115 (Fla. 4th DCA 2001) said that compliance with Florida Statute section 627.4137 is not a mere “technicality.” The court said that the legislature recognized the importance of a claimant’s access to this type of information in making settlement decisions.

The production of a policy limits affidavit is an essential term of a settlement.

In Cheverie, Solanje Cheverie’s husband, Carroll, died on November 7, 1998 as a result of injuries he sustained when Marshall Geisser, collided with his automobile on July 28, 1998.

Allstate told Cheverie’s attorney that the BIL limits were $100,000. Despite multiple requests by Cheverie, Allstate didn’t send the policy limits affidavit.

Cheverie sued Geisser. Geisser argued that since Allstate sent Cheverie a check for the $100,000 BIL limits, the case was settled. Thus, Geisser argued that Cheverie had lost her right to sue because Allstate had met Cheverie’s settlement demand.

Cheverie argued that there was no settlement because Allstate never sent the policy limits affidavit. (She also had other arguments that I won’t get into here.)

If Insurance Company Doesn’t Send Policy Affidavit, You May Be Able to Get More Than the Limits

The appeals court ruled that there was no settlement because Allstate, among other things, failed to send a policy limits affidavit. This allowed Cheverie to continue her lawsuit against Geisser.

If Cheverie were to get a verdict above $100,000, she could argue that Allstate acted in bad faith by failing to produce the affidavit. Allstate may then have to pay the Cheverie the amount that the jury awards. This could be a huge financial win for Cheverie.

The $3,841,989 verdict that I mentioned was in a wrongful death case brought by a spouse against Walgreens for pharmacy negligence. That wasn’t my case. Perhaps other Florida courts have awarded higher amounts.)

Thus, the fact that Allstate may have acted in bad faith, could have allowed Cheverie too get a verdict that is multiples of its insured’s $100,000 policy limits.

This could potentially put the insurance company on the hook for a judgment above their insured’s BIL policy limits. The Broward County Clerk of Court shows that a notice of settlement was filed in Cheverie on February 4, 2002.

I assume that the settlement was for more than the policy limits. Otherwise, I think that Cheverie would have taken the case to trial.

Thus, if a liable party has low policy limits, and an insurer doesn’t send you the policy affidavit after you’ve demanded it, it could expose the insurance company to bad faith.

The Insurance Disclosure Must List Any Other Known Insurance

Gira v. Wolfe, 115 So. 3d 414 (Fla. Dist. Ct. App. 2013) is another case where the court ruled that there was no settlement when an insurer didn’t send the request policy disclosure. Like in Cheverie, Gira could then argue that the insurer acted in bad faith.

This could allow Gira to collect more than the policy limits from the insurer if she got a verdict that was higher than the policy limits.

The Wolfes were insured under a policy issued by Southern-Owners Insurance Company that included bodily injury coverage. Southern-Owners is part of (a subsidiary) of Auto-Owners Insurance Company.

Gira’s claim against the Wolfes was assigned to Jeremy Moore, a claims representative employed by Auto-Owners.

Gira’s attorney sent a letter to Moore which requested “all the statements, documentation, and all of the information required to be disclosed pursuant to Section 627.4137.”

Moore sent a “Disclosure of Insured Information” which indicated that the Southern-Owners’ policy provided $50,000 coverage for bodily injury. The disclosure form further stated that other insurance which may be available to the above named insured which is known to Southern-Owners at this time is as follows.”

The space for other insurance to be listed was left blank. Moore enclosed a $50,000 policy limits check for Gira’s injury claim.

Gira’s attorney returned the check and release to Auto Owners. Gira then sent a letter to Moore requesting statements and all information required to be disclosed pursuant to Section 627.4137 Florida Statutes.

Again, Moore responded with a policy disclosure where the space for other insurance to be listed was left blank.

You May Be Able to Get More Than the Policy Limits if The Insurer Doesn’t Tell You About Other Insurance

As I stated earlier, the appeals court said that there was no settlement because Auto Owners didn’t meet Gira’s settlement conditions.

Thus, Gira may have had a bad faith case, and the ability to collect more than $50,000 from Auto Owners Insurance Company.

If the Insured Has High BIL Limits, You Don’t Have a Big Remedy

On the other hand, if the responsible party has high BIL limits, then failure to comply with 627.4137 doesn’t really impose a penalty on the insurer.

However, a claimant can file a consumer complaint against the insurer. It may get the insurer to provide this insurance information quickly.

Otherwise, the Florida Office of Insurance Regulation can fine the insurer if it doesn’t provide the policy affidavit to you.

Does an insured, or his or her insurance agent, have to disclose the name and coverage of each known insurer to the claimant and forward the request for info to all affected insurers?

Yes, if the claimant or the claimant’s attorney makes a written request. However, if they fail to disclose the info you have little recourse.

If the insured, or his or her insurance agent, forwards the request to the insurer, the insurer must then give the information required to the claimant within 30 days of receipt of such request.

Does the liability insurer’s statement need to be amended (updated) immediately upon discovery of facts calling for an amendment to such statement?

Yes. Florida Statute 627.4137(2).

Does a request made to a self-insured corporation pursuant to this section need to be sent by certified mail to the registered agent of the disclosing entity?

If you were in a rideshare accident, you should hire an Lyft or Uber accident lawyer.

Find out if I could be the lawyer for you

Complete this form to see if I could be the injury lawyer for you.

That’s the easiest and fastest way for me to see if I could be the lawyer for you.

📞 If you prefer, you can call us at 888-594-3577 to see if I can represent you if someone caused your injury in Florida, or on a cruise. You can call me any day of the year. (Note: The call is to see if I could be the lawyer for you, not to give you free advice.)

I will not become your attorney by you leaving a comment. There is a time limit to file a lawsuit. All comments will be public. This includes the name that you enter. I only represent people who were hurt in Florida or on a cruise ship; or if the injured person lives in Florida or a family member (in the case of a death) lives in Florida. This is because I am only licensed in Florida.

Leave a Reply